The scale-up flywheel

The scale-up flywheel

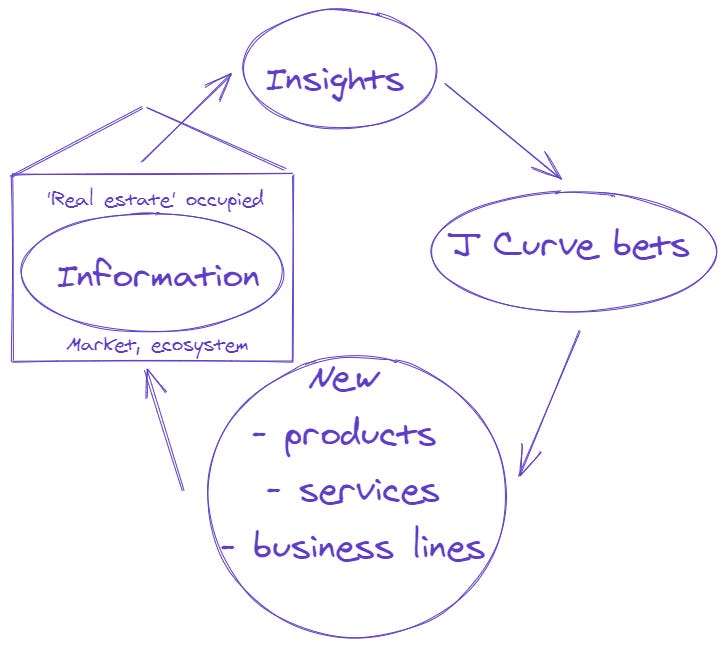

Information -> Insights -> J Curve bets = Breakout opportunities

The largest businesses are the result of aggregate bets made over time. And while you may only see or hear about the bet that becomes synonymous with the brand, it’s important to remember that the life of a business often evolves based on a history of trial and error.

Amazon went from a bookseller to an ‘everything store’ to ‘you can use our store to run your store’. (check out What exactly is Amazon?).

Airbnb went from spare mattresses on the ground to renting whole properties to providing multi-day experiences (including virtual experiences) for guests.

Uber grew its disrupting commuter service, from letting you hail a black limousine, to becoming the largest ride-hailing company to delivering food to your door (Uber’s delivery business is now larger than ride-hailing).

Square, having derived their name from selling square-shaped credit card readers, evolved to be the number one software finance app in the Appstore, with CashApp alone being valued at $40 billion.

So what can we learn from these evolutions?

That companies usually start serving a niche audience with a targeted product hook. Their user base starts to build, two outcomes usually happen, they start seeing their growth stall (invisible asymptotes) or they leverage their information machine and start to serve deeper much more valuable users and use cases.

The piece is the first in a series that will explore the various methods through which companies can evolve from being a one-trick pony to ladder up and increase their market share and creating demand by offering new products, services or entirely new business lines.

Even if they fail, the act of trying to launch new endeavours has proven to provide a significant advantage. It’s about building muscle memory so that when the next opportunity strikes you can move with maximum efficiency and skill.

I see a lot of people writing about the various stages from founder market fit -> product-market fit -> growth strategy market fit. This makes a ton of sense; going from 0-1 is like getting onto the beach at Normandy, a fight for survival ensues - but what happens once you get into position? Let’s explore places that might bear interesting answers and from which you can start making smart bets.

The basic evolution loop

What is an insight?

An insight, at its heart, is an idea - an idea that is usually earned or stumbled upon.

A discovery of such an insight can have a powerful propelling force for your destiny.

It could be a fundamental truth that powers the direction of your company, a new market for adjacent users of use cases, or new intel on why consumers are drawn to your company and you need to pivot to capture the market.

The advantage of being in any market is owning some form of theoretical real estate where you gather a flow of information. Information leads to insights.

Two things to note that we will explore later; 1) externally, there is better real estate to occupy and 2) internally, it is valuable to have a culture of free-flowing information and experimentation.

As a start-up, you are likely talking to many people about their problems and how those relate to your product. You talk to users and non-users and discover who really uses your product and why or why not. This leads to an information flow as illustrated below:

Take Square as an example - its initial goal was to increase access to the economy, which is why they made square readers for small or one-person businesses to accept payments.

Listen to Jack Dorsey talk about Square’s evolution from a card reader to payments provider.

“We weren’t expecting this, we thought we were just building a piece of hardware, to enable people to plug it into their phone and swipe a credit card and as then we talked with people, we found a consistent theme, they weren’t allowed to accept a credit card. There was a credit check waiting”.

Square listened to the market and realised they were inadvertently falling short of their mission, but they had an insight so they took a different approach: Create a system that lets people previously held back due to arbitrary rules to finally be able to accept credit cards and be included in the banking system. Instead of making these small retailers jump through credit hoops (remember to accept payments), they would onboard them immediately and monitor their behaviour from the subsequent transactions with machine learning. This opened up its market considerably, they had a strategic competitive advantage and have grown 10x or $75 billion (also thanks to Cash App) since 2017.

Insights can take time to develop, but you want to be in a position to surface them, act upon them and keep moving if things don’t work out. Here is Sam Hinkie, who served as the general manager of the Philadelphia 76ers and helped rebuild the organisation, in his resignation letter talking about innovation and insights. “Sadly, the first innovation often isn’t even that helpful, but may well provide a path to ones that are.”

What is a bet?

Due to my background in poker and trading, thinking in terms of bets comes naturally to me. However, it is best described by Annie Duke in her book with the same name.

We are most of our decisions cumulatively, we’re not betting against another person —we’re betting against all the future versions of ourselves that we are not choosing.

In this context, the essence of a bet is an experiment of a new initiative. That could be a new product, service or business. Think of it as a heavy A/B test.

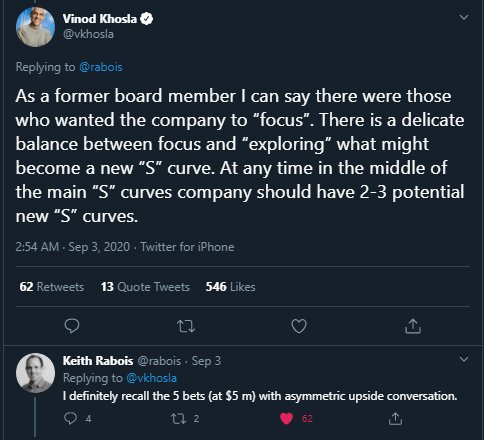

Here is Vinod Khosla the previous board member of Square and Keith Rabois former COO of Square talking about taking the Cash App bet and four others. (note Vinod calls is an S Curve instead of my usage of J).

There is a skill that companies need to build up and that is structuring the experiment for evaluation and comparison. They need to think through all the possibilities of the outcomes and start handicapping them in terms of probability of success and the financial results. This will to get the expected value or “weighted-average value for a distribution of possible outcomes” for that experiment.

If a company has excess resources and has the opportunity to take bets that have capped downsides, but potentially huge upsides, they should definitely look to increase their variance to unlock new sources of value.

Jeff Bezos talks about this in Amazon’s 2016 annual shareholder letter:

Given a ten percent chance of a 100 times payoff, you should take that bet every time. But you’re still going to be wrong nine times out of ten. We all know that if you swing for the fences, you’re going to strike out a lot, but you’re also going to hit some home runs.

Let’s take two examples:

Business option 1: There is a 25% chance of success to achieve a $20 million outcome- $5mm expected value

Business option 2: There is a 1% chance of success to achieve a $1 billion outcome- $10mm expected value

Both cost the same and take the same time to run, now which do you gave after if you can go after? Even though option 1 is 25x more likely to happen you should choose option 2. (This is simple but it’s good to build up intuition. It is better to think in terms of probabilities and outcomes, a few scenarios it’s rarely pass or fail).

This process will hopefully highlight to them that although something might be unlikely, the rewards are so great that it's worth pursuing.

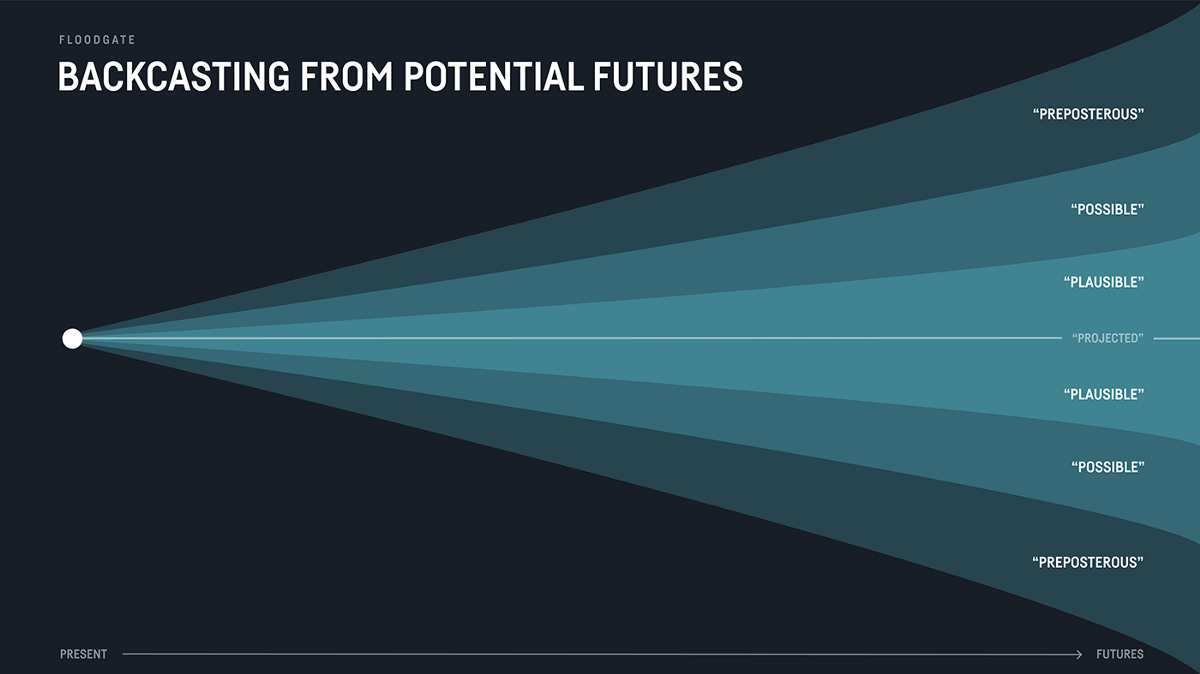

Mike Maples ‘How to build a breakthrough’ - provides an image to visualise part of this process in what he refers to as ‘backcasting’.

I mentioned Amazon which is famously a factory of bets. They leverage both their capital and inherent advantages of their scale and logistics network to place a multitude of strategic and high-upside bets. Amazon refers to itself as the best place in the world to fail, which I can only imagine as an employee, is quite a liberating experience to get air cover from the boss to swing big (as long as you have the data and a memo). After Amazon’s effort to launch the Fire phone failed quite spectacularly ($170mm, $83 million phones were collecting dust), Jeff Bezos said

“If you think [Fire Phone] is a big failure, we’re working on much bigger failures right now — and I am not kidding. Some of them are going to make the Fire Phone look like a tiny little blip.”

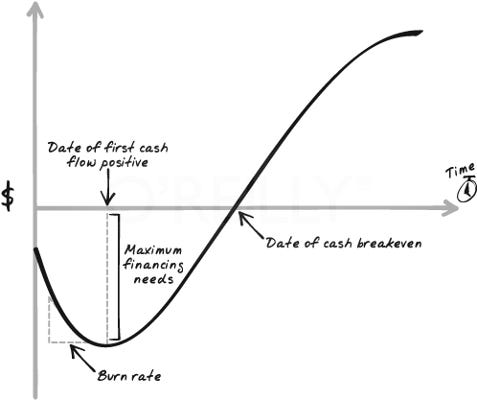

What is the J curve?

Combining all of these moving parts, the J curve - a theory, named after its shape, that broadly describes how an experiment will look, if it works out. It’s also a helpful measure of progress as the experiment plays out.

The first stage of the curve, the bottom of the J, represents the investment the company makes as time goes on. The bottom should be the company’s total investment amount.

The next stage is when the company start to gradually recoup the investment, and where the curve intersects with the X-axis, they have broken even on the bet. This is where the growth happens, or in other words, multiples of return on their bet start to build. The curve is not really representative of the real world in that you’d expect jagged periods of returns, but is instead a simplified time curve which represents a smooth linear curve, not exponential or changing (which seems to be most real-world experiences).

The takeaway to remember, however, is, if you see an opportunity that has asymmetric returns, you can start to work out the investment needed, and start to educate and quantify the upside (return profile) and time period needed. The eventual path may be different, but this framework will give you a report card for future reference and a benchmark for other opportunities.

Next

Now we have the understanding of the basic loop and its components, the next posts will explore the more practical and hopefully interesting, strategies to help generate those insights.

If you have any ideas on future trends or are building an early-stage startup — get in contact it would be great to hear from you.

A

Good article Poe with interesting thoughts. Look forward to reading more.